News

Dr. Abu-Ghazaleh underlined the most important amendments in the IFRS 2021, through this table:-

24-Mar-2022

AMMAN – HE Dr. Talal Abu-Ghazaleh, chairman of the International Arab Society of Certified Accountants (IASCA), announced the issuing of the latest Arabic translated version of the 2021 International Financial Reporting Standards (IFRS) in cooperation with the International Financial Reporting Standards Foundation (IFRS Foundation).

This edition is the sole official printed version of the consolidated text issued by the International Accounting Standards Board (IASB) on January 1, 2021, and was translated by the Saudi Organization for Certified Public Accountants (SOCPA).

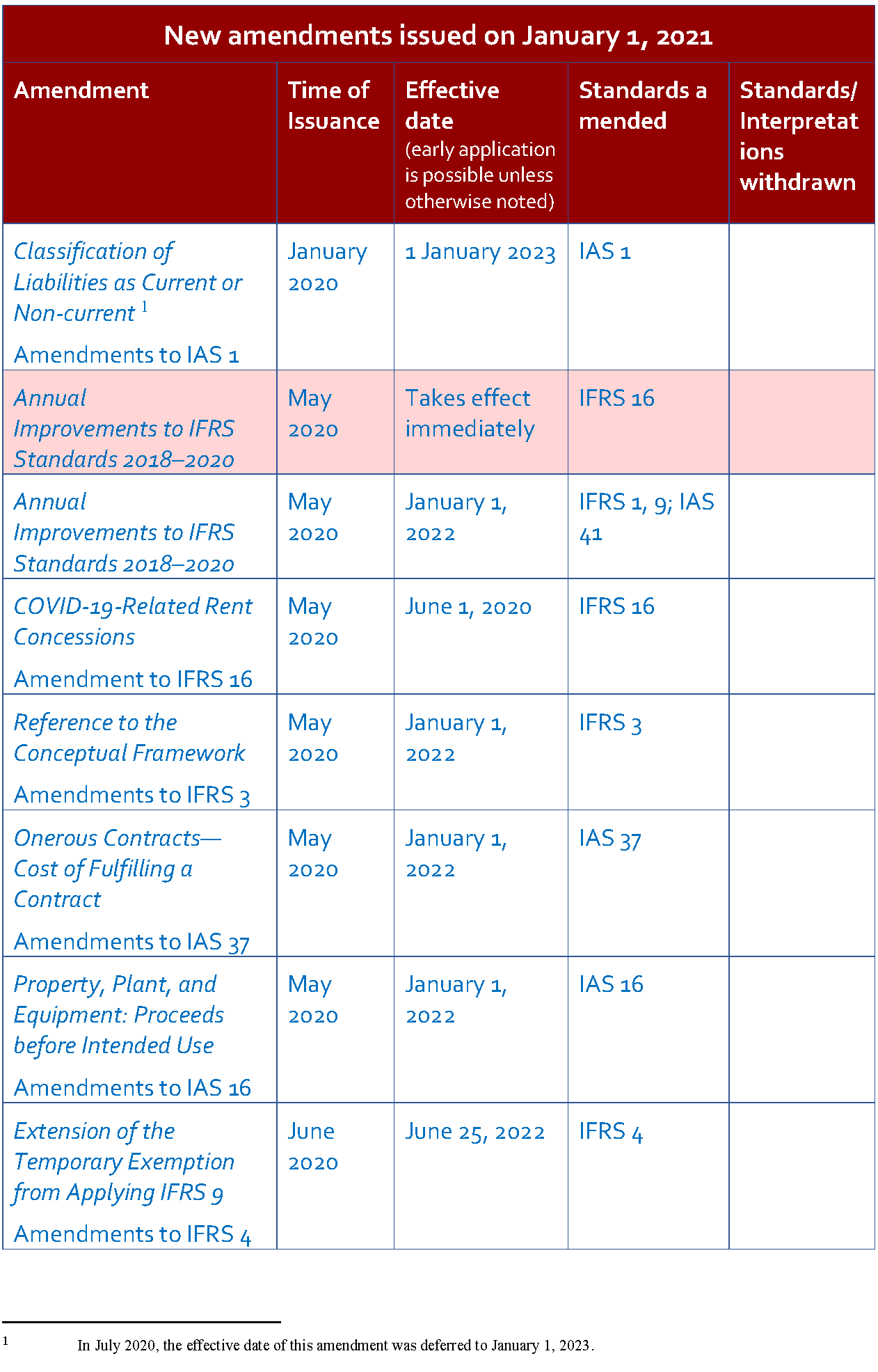

Dr. Abu-Ghazaleh underlined the most important amendments in the IFRS 2021, through this table:-

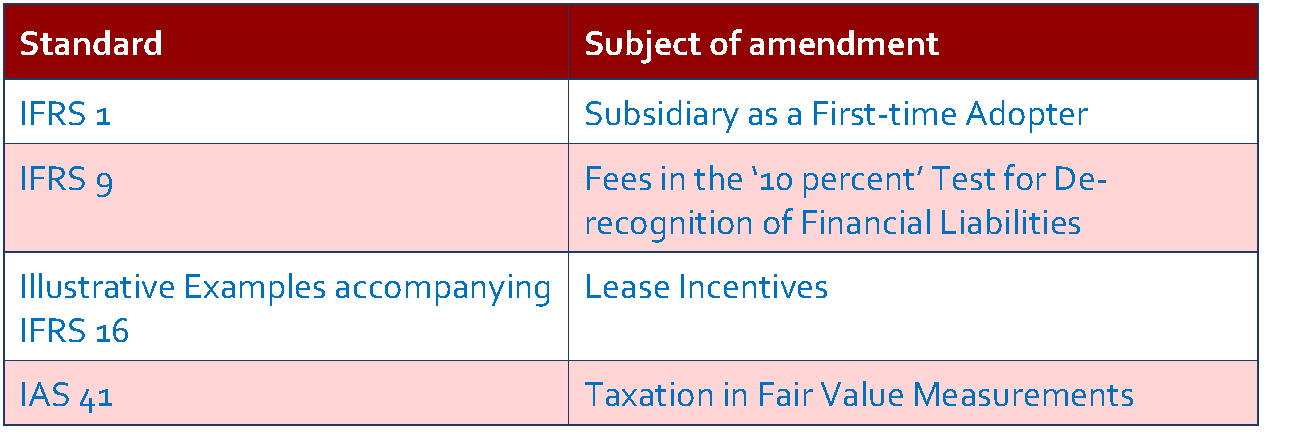

Annual Improvements to IFRS Standards 2018-2020

Annual Improvements to IFRS Standards 2018-2020 include the following amendments.

COVID-19-Related Rent Concessions

COVID-19-Related Rent Concessions, which amends IFRS 16, is effective from June 1, 2020, with earlier application permitted. The amendment permits lessees, as a practical expedient, not to assess whether rent concessions that occur as a direct consequence of the COVID-19 pandemic and meet specified conditions are lease modifications and, instead, to account for those rent concessions as if they were not lease modifications.

Onerous Contracts—Cost of Fulfilling a Contract

Onerous Contracts—Cost of Fulfilling a Contract amends IAS 37. The amendments clarify that for the purpose of assessing whether a contract is onerous, the cost of fulfilling the contract includes both the incremental costs of fulfilling that contract and an allocation of other costs that relate directly to fulfilling contracts.

Property, Plant, and Equipment: Proceeds before Intended Use

Property, Plant, and Equipment: Proceeds before Intended Use amends IAS 16. The amendments prohibit an entity from deducting from the cost of property, plant, and equipment amounts received from selling items produced while the entity is preparing the asset for its intended use. Instead, an entity will recognize such sales proceeds and related costs in profit or loss.

Extension of the Temporary Exemption from Applying IFRS 9

Extension of the Temporary Exemption from Applying IFRS 9, which amends IFRS 4, extends the temporary exemption from applying IFRS 9 by two years. It will expire for annual reporting periods beginning on or after January 1, 2023.

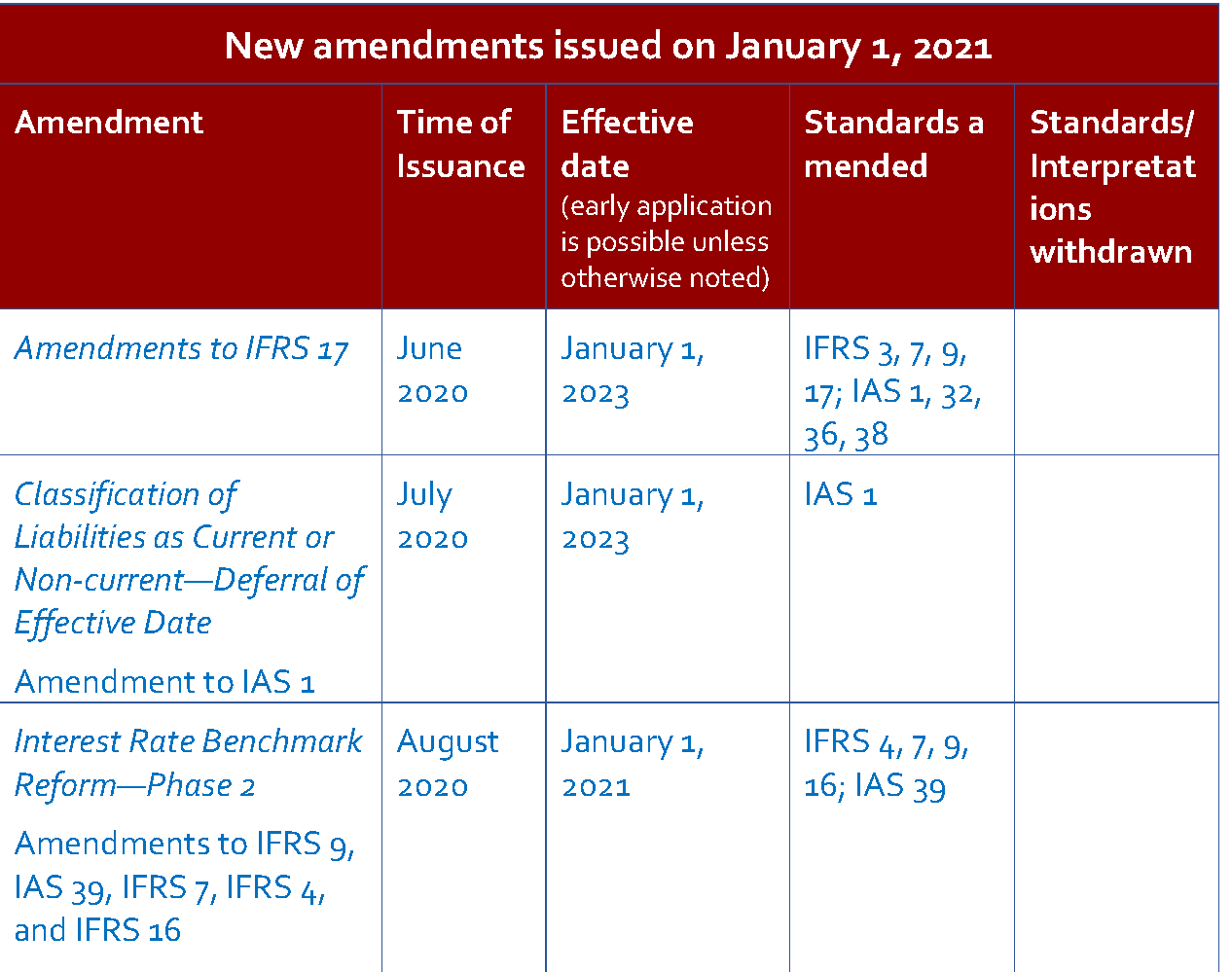

Amendments to IFRS 17

After the Board issued IFRS 17 in May 2017, it has been carrying out activities to support entities and monitor their progress in implementing the Standard. These activities helped the Board understand the concerns and challenges that some entities identified while implementing the Standard. The Board considered these concerns and challenges and decided to amend IFRS 17. The objective of the amendments is to assist entities implementing the Standard, while not unduly disrupting implementation or diminishing the usefulness of the information provided by applying IFRS 17.

IFRS 17, as amended in June 2020, is effective for annual reporting periods beginning on or after January 1, 2023.

Interest Rate Benchmark Reform—Phase 2

Interest Rate Benchmark Reform—Phase 2 (Phase 2 amendments) was issued in August 2020 and amends IFRS 9, IAS 39, IFRS 7, IFRS 4, and IFRS 16. The Phase 2 amendments address issues that might affect financial reporting during the reform of an interest rate benchmark, including the effects of changes to contractual cash flows or hedging relationships arising from the replacement of an interest rate benchmark with an alternative benchmark rate. The objectives of the Phase 2 amendments are to:

• Support companies in applying IFRS Standards when changes are made to contractual cash flows or hedging relationships because of the reform; and

• assist companies in providing useful information to users of financial statements.

It is worth mentioning that the International Arab Society of Certified Accountants (IASCA) signed a cooperation agreement with the IFRS Foundation to reprint, publish, and distribute the IFRS 2019 and the International Standards in Small and Medium-sized Enterprises 2019 books; accordingly, the Society will distribute the two publications to all Arab countries. The 15-year of mutual cooperation between the Society and the IFRS indicates the keenness of IASCA to serve the accounting profession and professionals at regional and global levels.